As a small business owner, staying informed about tax deductions can significantly impact your bottom line. Understanding the inflation-adjusted standard deduction for 2025 and 2026 is crucial. This change, based on the Chained Consumer Price Index, could alter your tax planning strategy. By familiarizing yourself with these adjustments, you can maximize your benefits and potentially save money.

Understanding Inflation-Adjusted Standard Deductions

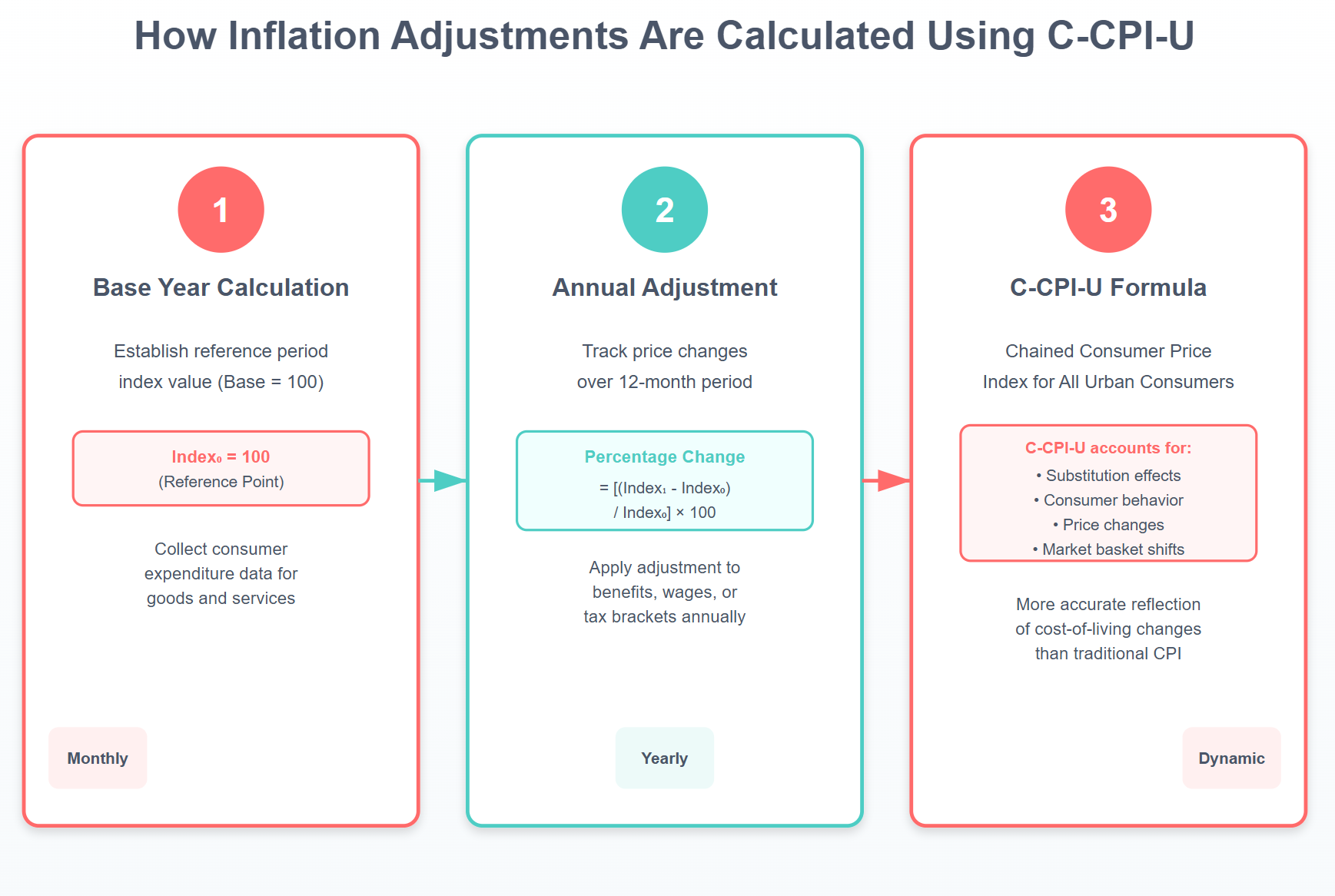

Inflation-adjusted deductions are designed to offset the effects of inflation. Each year, the IRS recalibrates tax brackets and standard deductions accordingly. This adjustment helps maintain the purchasing power of deductions over time. For instance, if inflation increases, so does your standard deduction.

How Does It Affect You?

For 2025 and 2026, the IRS will adjust the standard deduction based on the Chained Consumer Price Index. This index measures the cost of living more accurately than traditional methods. Consequently, you might see a rise in your standard deduction, which can lower taxable income. Learn more about the Chained Consumer Price Index here.

How Inflation Adjustments Are Calculated Using C-CPI-U

Preparing for Changes

To leverage these changes, start by reviewing your current tax strategy. Analyze how adjustments in the standard deduction will impact your taxable income. For example, if your business expenses are close to the deduction threshold, this adjustment might push you below it, increasing your tax savings. The Standard deduction “so much of” rule under § 63 can provide additional insights for this analysis.

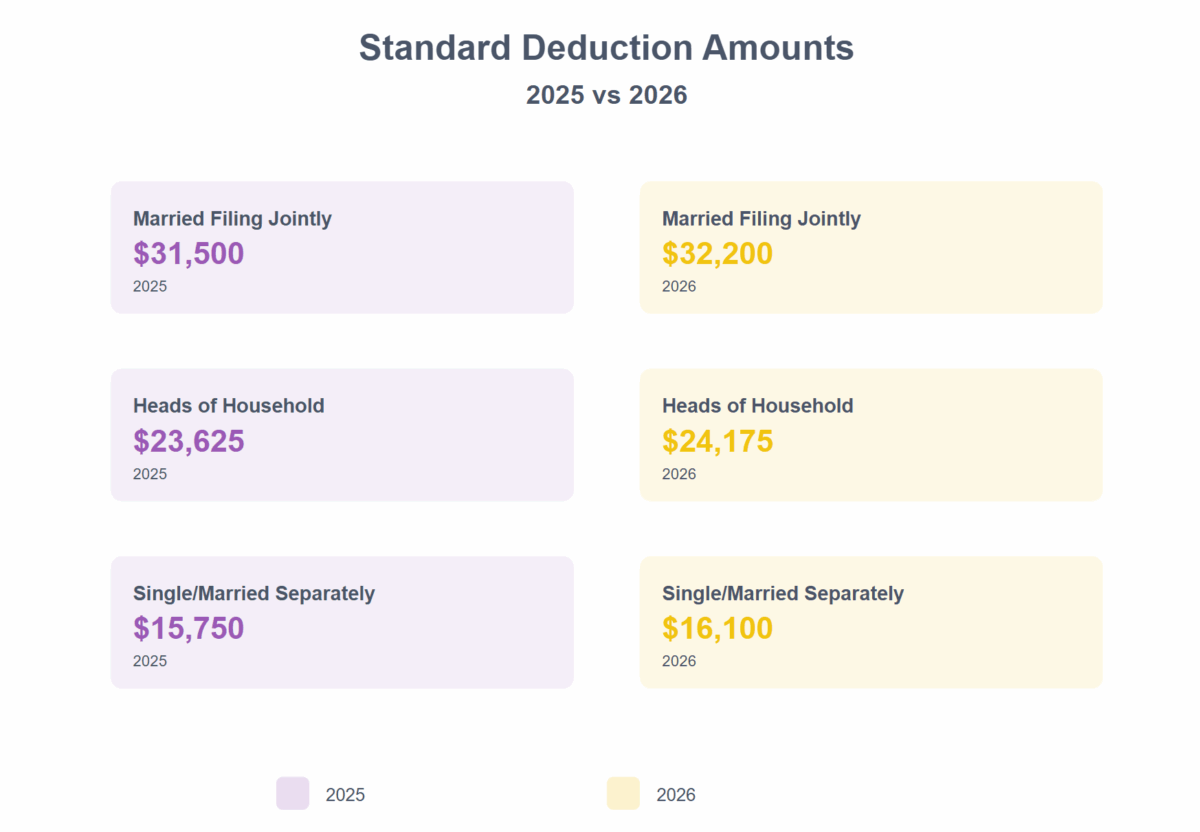

Standard Deduction Amounts for 2025 vs 2026

For tax year 2025, the standard deduction amounts are:

- Married individuals filing jointly and surviving spouses: $31,500

- Heads of household: $23,625

- Single taxpayers and married individuals filing separately: $15,750

For tax year 2026, the standard deduction amounts are:

- Married individuals filing jointly and surviving spouses: $32,200

- Heads of household: $24,175

- Single taxpayers and married individuals filing separately: $16,100

Practical Tips

- Review Past Returns: Look at your tax returns from the past few years. Identify patterns and areas where the increased deduction can be beneficial.

- Consult a Tax Professional: Engaging with a tax advisor can provide tailored insights. They can help you understand how these changes affect your business specifically.

- Adjust Quarterly Estimates: If you’re already making quarterly tax payments, consider adjusting these estimates according to the new deduction amounts.

Transitioning Smoothly

By planning ahead, you can transition smoothly into these new standards. It’s essential to stay proactive and adjust your strategy as needed. Additionally, staying informed about IRS updates ensures you’re never caught off guard. Visit the IRS official website for the latest updates.

🚨Free Slide Deck on Maximizing Tax Benefits

Leveraging IRS Resources

IRS Revenue Procedures

The IRS regularly releases revenue procedures that provide guidance on how to apply these changes. These documents are invaluable resources for understanding new tax rules. For detailed guidance on the upcoming changes, refer to the Rev. Proc. 2025‑32, which outlines the IRS revenue procedure for inflation adjustments for tax year 2026.

How to Use These Resources

Familiarize yourself with relevant IRS publications. These include detailed explanations and examples. Moreover, they often contain useful FAQs that can clarify common concerns.

Actionable Steps

- Subscribe to IRS Updates: Signing up for updates from the IRS can keep you informed about any further changes.

- Utilize IRS Tools: The IRS provides various online tools to help calculate your deductions and understand your obligations.

🤔 Quiz Yourself on Standard Tax Deductions

Conclusion: Taking Control of Your Tax Strategy

In conclusion, understanding the inflation-adjusted standard deduction for 2025 and 2026 is critical for optimizing your tax strategy. By staying informed and proactive, you can leverage these changes to your benefit.

Next Steps

- Educate Yourself: Continue learning about tax changes that affect your business.

- Plan Ahead: Implement the strategies discussed to adjust your tax planning accordingly.

- Seek Professional Advice: Don’t hesitate to reach out to a tax professional for personalized guidance.

By taking these steps, you can ensure that you’re maximizing your tax benefits and positioning your business for financial success. Remember, informed planning is the key to effective tax management.